Buying Property in Spain Costs - A Complete Buyer's Guide

So, you're planning to buy a property in Spain. Fantastic! Amidst the excitement of browsing villas and apartments, the biggest question that always comes up is, "What's this really going to cost me?"

The short answer, and the golden rule we tell all our clients, is to budget an extra 10-15% on top of the property's purchase price. This isn't just a rough guess; it’s a realistic figure that covers all the essential taxes and fees, ensuring you’re financially prepared for the entire journey from offer to completion.

Your Essential Spanish Property Cost Checklist

It’s incredibly easy to get swept up by the advertised price of your dream home on the coast. But the reality is, that number is just the starting point. To move forward with total confidence and avoid any unwelcome surprises, you need to understand the full picture.

Think of it like buying a car. The price you see on the windscreen is never the final figure you pay. You still have taxes, registration, and insurance to sort out before you can legally drive it off the forecourt. It’s exactly the same with Spanish property; the costs extend well beyond the agreed sale price to include mandatory government taxes, legal services, and administrative fees.

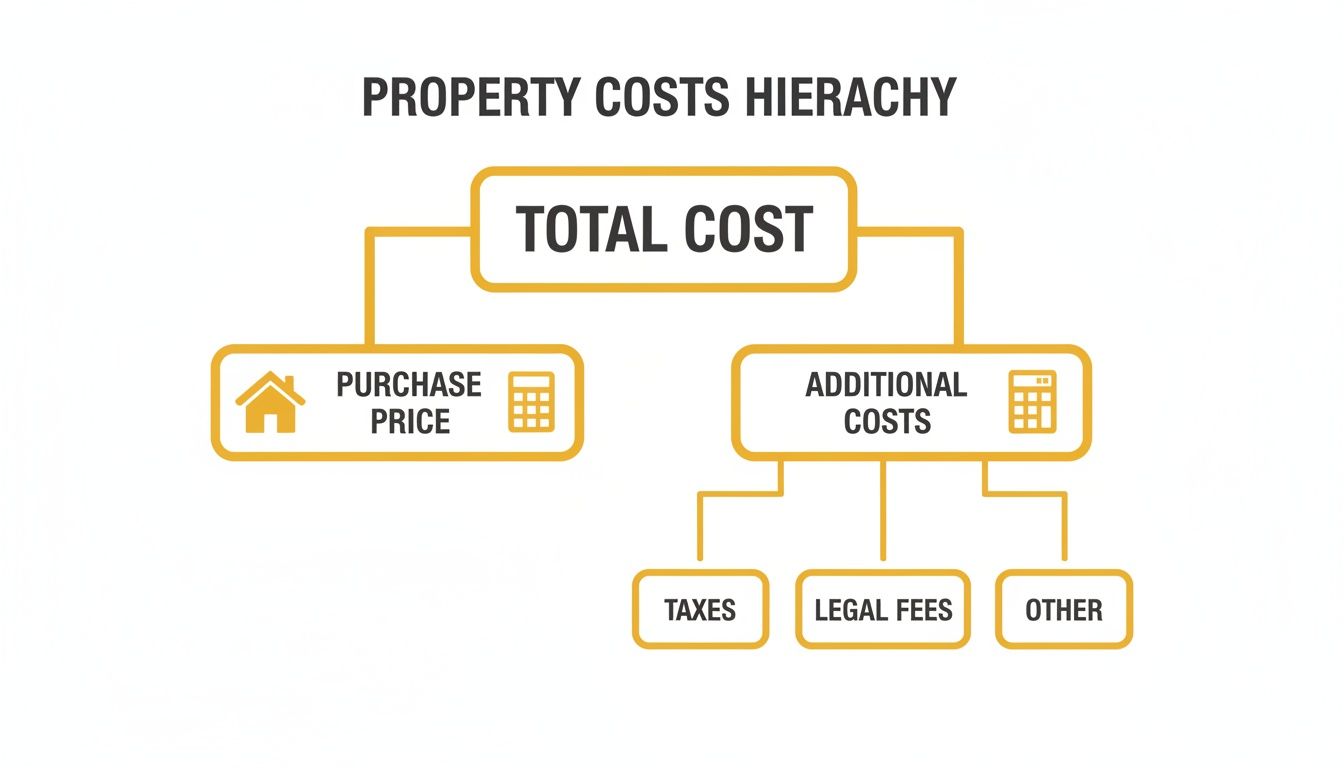

Mapping Out Your Total Investment

Getting your head around this 10-15% buffer is vital. It’s not an arbitrary figure—it's a reliable estimate built from a combination of charges that every single buyer will face. When you break them down, what seems like a daunting number becomes a simple, manageable checklist.

This flowchart gives you a clear visual of how your total investment is structured, separating the main purchase price from all the necessary add-ons.

As you can see, your total financial commitment is the sum of the property's price plus these associated costs, which mainly fall into three buckets: taxes, legal fees, and other administrative charges.

Key Takeaway: Budgeting for this extra 10-15% isn't just a good idea; it's a fundamental step for a successful purchase. Failing to have these funds ready can stall your plans or even jeopardise the entire deal.

Quick Breakdown of Spanish Property Purchase Costs

To give you a clearer overview, we've put together a quick summary of the typical costs you should expect. Just remember, these are solid estimates, but the exact percentages can shift a little depending on the property’s value and, importantly, the region in Spain where you choose to buy.

| Cost Component | Estimated Percentage of Purchase Price |

|---|---|

| Property Transfer Tax (ITP) or VAT (IVA) | 7-10% |

| Stamp Duty (AJD) - for new builds only | 1-1.5% |

| Notary & Land Registry Fees | 1-2.5% |

| Legal Fees (Lawyer/Abogado) | 1-2% |

These are the core expenses you’ll encounter. In the following sections, we'll dive deeper into what each of these means for your budget, so you know exactly what to prepare for.

Decoding Property Taxes: New Builds Versus Resales

When you're working out your budget for buying a property in Spain, the single biggest chunk you'll need to account for—after the property price itself—is the tax. This is where a lot of buyers can get tripped up, but it's actually quite straightforward once you understand one key difference: are you buying a brand-new home from a developer, or a resale property from a previous owner?

The path you choose determines which tax you'll pay. It helps to think of it like buying a car. A shiny new one straight from the showroom has Value Added Tax (VAT) included, whereas a second-hand car from a private seller involves a completely different transfer tax. Spanish property works in a very similar way. Getting this right from the start is absolutely crucial for your budget.

Knowing which tax applies to your dream home is the first step to creating a realistic and stress-free financial plan. So, let’s break down both scenarios.

The New-Build Premium: VAT and Stamp Duty

If you've set your heart on a pristine, off-plan villa or a key-ready apartment that has never been lived in, you’ll be looking at two separate taxes.

First up is the Value Added Tax, known in Spain as IVA (Impuesto sobre el Valor Añadido). Because this is a national tax, the rate is the same no matter where you buy in the country. For residential properties, IVA is a flat 10% of the purchase price.

But it doesn't stop there. On top of IVA, new-build purchases also attract Stamp Duty, or AJD (Actos Jurídicos Documentados). This tax covers the legal documentation of the sale and is managed by Spain's regional governments. This means the rate can change depending on the property's location.

- What it is: A tax on brand-new properties, much like VAT on new goods.

- What you pay: A fixed 10% IVA on the purchase price.

- Plus: A variable AJD (Stamp Duty), which is typically between 1% and 1.5%.

When all is said and done, for a new-build property, you should budget for a total tax bill of roughly 11% to 11.5% of the purchase price.

The Resale Route: Understanding ITP

If you're buying a pre-owned home, the tax structure is much simpler. You won't pay any IVA or AJD. Instead, you'll pay a single tax known as the Property Transfer Tax, or ITP (Impuesto de Transmisiones Patrimoniales).

This tax is the biggest variable when calculating the costs of buying property in Spain, as the rate is set independently by each of Spain's 17 autonomous communities. The percentage you pay depends entirely on where the property is located, not where you are from.

For instance, the ITP rate in the Valencian Community (home to the ever-popular Costa Blanca) is a flat 10%. But head over to Andalusia (home to the Costa del Sol), and you'll find a sliding scale system. Go to Madrid, and it’s a flat 6%. This regional difference can easily mean a saving of thousands of euros on properties with the same price tag, making it a critical factor in your budgeting.

This variation really underlines how important it is to get local, expert advice to fully understand the specific costs in your chosen area.

To make it crystal clear, here’s a simple comparison of the main taxes you’ll face:

Comparing Taxes: New Build vs Resale Property

| Tax/Fee | New-Build Property | Resale Property |

|---|---|---|

| Primary Tax | IVA (Value Added Tax) at a fixed 10% | ITP (Property Transfer Tax) at a variable 7%-10% |

| Secondary Tax | AJD (Stamp Duty) at a variable 1%-1.5% | None |

| Total Tax Estimate | ~11.5% of the purchase price | ~10% of the purchase price (in the Valencian Community) |

As you can see, the route you take—new build or resale—has a direct and significant impact on your final tax bill.

The Non-Negotiables: Notary and Land Registry Fees

Whether you buy a new build or a resale, two final costs are completely unavoidable: the Notary fees and the Land Registry fees. These aren't taxes, but official charges for the essential legal services that make your ownership official and secure.

The Notary (Notario) is a public official who witnesses the signing of the final deed of sale (Escritura de Compraventa), verifies everyone's identity, and ensures the entire transaction is legally watertight. Their fees are set by a national scale but can vary slightly depending on the property's value and how complex the deed is.

The Land Registry (Registro de la Propiedad) is where your ownership is officially recorded for all to see. This is the crucial final step that legally protects your title to the property. The fees for this service are also based on a sliding scale linked to the property price.

Combined, you should budget somewhere between 1% and 2.5% of the purchase price to cover both the Notary and Land Registry fees. It’s a small price to pay to know your new Spanish home is officially and legally yours.

Assembling Your Team: Professional Fees and Legal Costs

Beyond the government taxes, buying a property in Spain means bringing in a team of skilled professionals whose entire job is to protect your interests. It’s easy to see their fees as just another expense, but in reality, it’s a crucial investment in a smooth, secure, and legally sound purchase. These are the experts who ensure every detail is correct, saving you from headaches and potential pitfalls down the line.

Trying to navigate the legalities and negotiations of a foreign property market on your own would be a monumental task. That’s why assembling a reliable team from the very beginning is one of the most important steps you can take. These fees are a core part of the overall buying property in spain costs and should be planned for right alongside the main taxes.

The Indispensable Role of Your Lawyer

Hiring an independent lawyer, or abogado, is non-negotiable. Seriously. Think of them as your personal advocate in the transaction, working exclusively for you—not the seller, not the agent, just you. Their primary role is to conduct thorough due diligence, making absolutely certain the property you want to buy is free of any hidden debts or legal problems.

Here’s a critical detail about Spanish law: debts are attached to the property itself, not the previous owner. This means an unpaid mortgage, a forgotten utility bill, or an outstanding community fee could legally become your responsibility after the sale. Your lawyer prevents this nightmare scenario by meticulously checking the Property Registry (Registro de la Propiedad) and verifying all legal paperwork.

Key Insight: Your lawyer is your shield. They confirm the seller is the legal owner, that all building permits are in order, and that there are no outstanding charges against the property—a service that provides invaluable peace of mind.

Legal fees are usually calculated as a percentage of the purchase price. You should budget between 1% and 2% of the property’s value for your lawyer’s services, though some may offer a fixed fee for more straightforward transactions.

Understanding Real Estate Agent Commissions

One of the first questions international buyers ask is about real estate agent fees. Here’s the good news: in Spain, the commission is almost always paid by the seller, not the buyer. This fee, which generally ranges from 3% to 6% of the final sale price, is simply taken from the proceeds of the sale.

This structure means you, the buyer, get to benefit from the agent’s local knowledge, property portfolio, and negotiation skills without having to pay them directly. The seller covers this cost as compensation for the agent’s work in marketing the property and finding the right person to buy it.

- Lawyer (Abogado): Budget 1% to 2% of the purchase price for their essential due diligence and legal representation.

- Real Estate Agent: The seller typically pays their commission, so this is not usually a direct cost for you as the buyer.

By understanding these professional fees, you can assemble a team that will guide you confidently through the purchase. Their expertise is what transforms a complex process into a secure investment, ensuring your new life in Spain starts on the strongest possible footing.

Sorting Out Mortgage and Financing Charges in Spain

For many international buyers, a mortgage is the key to unlocking their dream home in Spain. But while a loan opens up incredible possibilities, it’s important to remember that it comes with its own set of costs. These aren't hidden fees, but rather the standard charges for getting everything set up.

Think of it as the administration side of your home loan. Just like you pay taxes and legal fees for the property itself, the bank has specific charges for arranging the mortgage. Getting these budgeted for from the start is crucial for a smooth purchase, preventing any last-minute financial surprises. Let’s break down exactly what you should expect.

The Mandatory Property Valuation

Before any Spanish bank will lend you a cent, they need to know what the property is actually worth. This is where the property valuation, or tasación, comes in. The bank will hire an independent, officially registered appraiser to inspect the property and produce a formal valuation report.

This isn't just a box-ticking exercise. The bank's mortgage offer is based on this official figure, not necessarily the price you've agreed with the seller. For non-residents, Spanish banks will typically lend 60-70% of the tasación value. So, if the valuation comes in lower than the purchase price, you’ll need to find a larger deposit to cover the difference. It’s a common scenario, so it pays to be prepared.

- What it is: A professional appraisal of the property's market value, required by the bank.

- Who pays: You, the buyer.

- Estimated Cost: Usually somewhere between €300 and €600, depending on the property's size and value.

Making Sense of Bank Arrangement Fees

Once the valuation is done and you've accepted the mortgage offer, the bank will charge an arrangement fee, known as the comisión de apertura. This is a one-off payment to cover the bank's administrative work in setting up your loan.

In the past, these fees could be quite hefty. Thankfully, Spanish mortgage laws have been updated to give buyers more protection. Nowadays, the fee is typically between 0.5% and 1% of the total mortgage amount. In a competitive market, some banks might even waive it completely to win your business, so it's always worth asking your advisor about this when you're comparing offers.

Good to Know: While the bank now covers the notary, land registry, and stamp duty costs for the mortgage deed itself (this is separate from the property purchase taxes), you, the buyer, are still responsible for the valuation and arrangement fees.

Understanding the Euribor and Your Interest Rate

Your mortgage interest rate in Spain will either be fixed (tipo fijo) or variable (tipo variable). A variable rate is directly linked to the Euribor (Euro Interbank Offered Rate), the benchmark rate for lending between European banks. If the Euribor goes up, so will your monthly payments; if it falls, you'll pay less. Getting your head around this is vital for long-term financial planning.

The Euribor's movement has a real impact on the property market. With current forecasts predicting a fall in the Euribor, financing is becoming more accessible for international buyers. This, in turn, is helping to fuel demand and support property values, with some analysts predicting prices on the Costa Blanca could rise by 5-8%. You can read more about the Spanish property market and house prices to get a fuller picture of these trends.

Finally, keep in mind that banks will often tempt you with a better interest rate if you also take out other products with them, such as:

- Home Insurance (Seguro de Hogar): This is compulsory for any property with a mortgage.

- Life Insurance (Seguro de Vida): Often required to cover the outstanding loan amount if the worst should happen.

While bundling these can look attractive on paper, always compare the total cost. Sometimes it's cheaper to source these products elsewhere, even with a slightly higher mortgage rate. It’s all about finding the best overall value for your situation.

Budgeting for Life in Spain: What Are the Ongoing Costs of Ownership?

Getting the keys to your new Spanish home is a massive moment, but your financial planning doesn't stop there. The true joy of living in Spain comes from enjoying your property without worrying about money, and that means getting a handle on the regular running costs right from the start.

These ongoing expenses are a core part of the total buying property in spain costs. Think of it this way: the purchase price gets you in the door, but these annual costs are the subscription fee for your new Mediterranean lifestyle. Factoring them into your budget from day one is the secret to making your dream sustainable for the long haul.

Your Annual Real Estate Tax or IBI

The biggest yearly cost you'll have is the Real Estate Tax, known everywhere in Spain as IBI (Impuesto sobre Bienes Inmuebles). It’s basically the equivalent of the UK's council tax and you'll pay it directly to your local town hall (Ayuntamiento).

How much you pay is based on the property’s official taxable value, the valor catastral, which is nearly always lower than what you actually paid for it. The tax rate is set by the local council and usually falls somewhere between 0.4% and 1.1% of that valor catastral. For an apartment, your IBI bill might be a few hundred euros a year, while a large villa could easily run into a few thousand.

Community Fees for Shared Living

If your property is part of a shared community or urbanización—which is the case for most apartment blocks and many villa developments—you'll pay community fees, or gastos de comunidad. These fees are what keep all the shared facilities that make these places so appealing in top condition.

Your contribution goes into a pot managed by the community of owners to cover things like:

- Keeping the swimming pools and gardens looking pristine

- Cleaning communal hallways and entrances

- Electricity for lighting shared spaces

- Lift maintenance and any necessary repairs

- Security guards or systems

These are typically paid monthly or quarterly and can be anything from €50 to over €200 per month, all depending on the quality and number of amenities on offer.

Utilities and Other Essentials

Just like back home, you'll need to budget for your standard household bills. This means electricity (luz), water (agua), and internet. The rates can vary, but it's a good idea to set aside around €100 to €200 per month to cover the basics.

On top of that, every household pays an annual waste collection tax, the tasa de basura. This is another small local tax paid to the town hall, and it’s usually a pretty modest amount, often less than €100 per year. And of course, comprehensive home insurance (seguro de hogar) is an absolute must for peace of mind—it's also a legal requirement if you have a mortgage.

A Quick Word on Non-Resident Income Tax

This is a cost that often catches non-resident owners by surprise. Even if you never rent out your property, the Spanish taxman considers you to have a "deemed" rental income just from owning a second home here.

This tax is called Impuesto sobre la Renta de No Residentes (IRNR). It's calculated on a tiny percentage of your property’s valor catastral, so the final bill is usually very manageable—often just a few hundred euros a year. But it is a legal requirement you need to take care of.

The Spanish property market is hotter than ever, attracting buyers from all over the globe, with places like the Costa Blanca seeing incredible growth. Recent figures show property prices in the Alicante province shot up by 17.0% year-on-year, thanks to huge demand in hotspots like Torrevieja and Orihuela Costa. This booming market really highlights why it's so important to work with experts like AP Properties Spain, who can give you the end-to-end support you need for a secure investment. You can read the full analysis of the Spanish real estate market for a deeper dive into these trends.

Finding Your Dream Home with Financial Confidence

Navigating the costs of buying a property in Spain can feel like a maze at first, but it doesn't have to be. The journey to your dream home is about more than just finding the perfect view; it's about making a smart, secure investment with total clarity on every single euro. By now, you'll see that the extra 10-15% isn't some random figure—it's a clear, manageable checklist of taxes and professional fees.

This financial preparedness is the bedrock of a successful purchase. It transforms what could be a stressful process into an exciting, confident step towards your new life in Spain. Working with a trusted advisor simplifies this journey, ensuring every legal and financial detail is handled meticulously for you.

From Complex Costs to Clear Steps

The real takeaway here is that every cost, from the ITP tax to notary fees, is predictable. With the right guidance, you can budget for it all. A knowledgeable partner doesn't just find you a property; they lay out a clear roadmap of the buying property in Spain costs, making sure there are no surprises along the way. Think of them as your advocate, managing negotiations and coordinating with lawyers to protect your interests at every turn.

This expert support is what provides true peace of mind. It allows you to focus on the excitement of finding your perfect home, knowing the intricate financial details are in safe, experienced hands.

This level of professional guidance is especially vital in a dynamic market. For instance, in 2024, house prices in Costa Blanca are averaging €2,645.27 per square metre, a significant jump reflecting surging international demand. This upward trend, driven by a shortage of supply rather than speculation, shows the value of securing a property before prices climb even higher.

Working with a consultancy like AP Properties Spain—recognised as the Best Luxury Boutique Real Estate Consultancy in Costa Blanca for 2024 and 2025—ensures you can act decisively in this competitive environment.

Take the Next Step with Confidence

Understanding the costs is the first step, but what truly matters is applying them to your personal situation. Your dream home, your budget, and your investment goals are unique, and your financial plan should be too.

Ready to turn your dream of owning a home in Spain into a reality? It all begins with a simple conversation.

Contact AP Properties Spain today for a personalised consultation. We will provide a detailed cost breakdown tailored to your specific needs, giving you the clarity and confidence to move forward. Let us help you make your Spanish property aspirations a successful and rewarding investment.

Your Questions Answered: Budgeting for Your Spanish Property

When you're thinking about buying a property in Spain, the financial side of things can feel like a bit of a puzzle. We get it. To help you see the full picture and plan with confidence, we’ve put together straightforward answers to the questions we hear most often from international buyers.

How Much Cash Do I Really Need Upfront?

This is probably the most critical question. For non-residents, Spanish banks will generally lend you 60-70% of the property's official value. That means you need to have the other 30-40% ready as a deposit.

But here’s the key part many people miss: that deposit doesn't cover the taxes and fees. You'll need an extra 10-15% of the purchase price on top of the deposit to handle all those costs. So, before you even start looking, a good rule of thumb is to have 40-55% of your target property price available in cash.

Can I Get a Fixed-Rate Mortgage in Spain?

Yes, absolutely. Spanish banks offer both fixed-rate (tipo fijo) and variable-rate (tipo variable) mortgages, and fixed-rate deals are a very popular choice for international buyers. Why? Because it locks in your monthly payment for the life of the loan, making budgeting simple and predictable. No surprises.

A variable-rate mortgage is tied to the Euribor index, which means your payments will go up or down with the market. The right choice really comes down to your personal financial situation and how comfortable you are with a bit of risk.

What on Earth is a NIE Number, and Do I Actually Need One?

Think of the NIE (Número de Identificación de Extranjero) as your official ID for anything financial in Spain. It's a unique tax number for foreigners, and you simply cannot move forward without it.

You’ll need it to buy a property, open a Spanish bank account, connect your electricity and water, or even purchase a car. Getting your NIE is one of the very first things you need to do. A good lawyer can sort this out for you, making it a painless step in the process.

Expert Tip: Don't put off your NIE application. It’s the foundation for everything that follows, and getting it sorted early keeps the whole process running smoothly. It’s one of the first signs of a well-planned purchase.

Are Property Prices Negotiable in Spain?

Generally, yes—especially when it comes to resale properties. How much wiggle room you have often depends on things like how hot the local market is, how long the property has been for sale, and the seller’s own circumstances. In high-demand areas like the Costa Blanca, there might be less flexibility.

New-build properties, on the other hand, usually have fixed prices set by the developer, so there’s no room for negotiation there. This is where having a skilled agent in your corner is priceless. They know the local market inside out and can advise on a realistic offer, handling the negotiations to get you the best possible deal.

Share